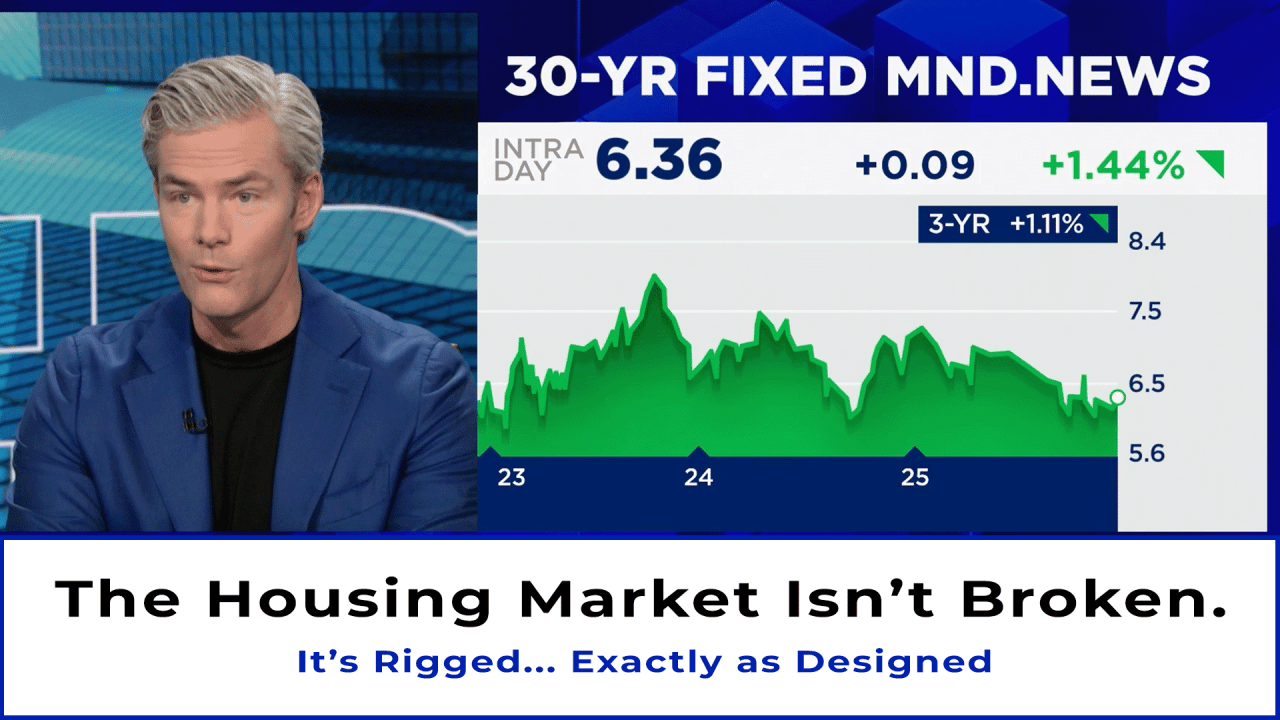

Every day I hear the same narrative: “The U.S. housing market is broken.”

It is always followed by hopeful predictions like “Affordability will come back” or “Prices will normalize soon.”

Let me be blunt: none of that is true.

The U.S. housing market isn’t broken.

It’s rigged.

And it has been since 1997, by design. We created a system that rewards scarcity, protects existing homeowners, and punishes mobility. Prices are not high by accident. They are high by policy.

To understand how we got here, you need to understand the single most important, and quietest, shift in modern American homeownership.

1997: The Year We Financialized the American Home

In 1997, Congress fundamentally rewrote the rules by creating the modern home sale capital gains exclusion, Section 121 of the IRS code. This allowed homeowners to keep $250,000 of profit tax free ($500,000 for married couples) when they sell their primary residence.

No income limit. No age requirement. No cap on how many times you can use it, as long as you meet the “2 out of 5 years” rule.

In one stroke, the American home stopped being just shelter.

It became the most powerful tax advantaged investment vehicle in the country.

Before 1997, Housing Was About Living. After 1997, It Became About Leveraging.

Before 1997:

• You could defer taxes only by buying a more expensive home • “Trading up” happened slowly, over decades • Appreciation was nice, but not the central purpose

After 1997:

• Tax free profit became a cornerstone wealth strategy • The incentive to stay put and wait for appreciation skyrocketed • Homeownership became a tax shelter

Layer on top of that:

• 30 year fixed mortgages • Local zoning that restricts supply • The lowest interest rates in recorded human history • Institutional capital entering the single family market

…and you get the system we have today. Not broken. Engineered.

What Happened Next

Home prices didn’t just rise, they disconnected from economic fundamentals.

In 1997, the median existing home cost $124,100. Today it is roughly $430,000. New homes saw the same acceleration, rising from $143,000 to over $500,000.

That’s not normal appreciation. That’s asset inflation layered on top of scarcity and policy distortion.

And it created the condition we’re living with today: the market isn’t heading toward a “crash,” it’s heading toward a freeze.

Sellers are locked in by 3 percent mortgages and tax incentives that reward staying put. Buyers can’t afford to buy. Investors have no reason to sell. Builders struggle to profitably produce entry level homes.

This isn’t a cyclical problem. It’s a structural one.

America Doesn’t Have a Housing Shortage. It Has a Permission Shortage.

We have the land. We have the builders. We have the demand.

What we lack is the political will to unlock supply.

When the majority of voters are homeowners whose largest asset keeps rising, the incentive to change the rules simply doesn’t exist. And so the system continues to do exactly what it was designed to do: protect existing wealth and limit new access to it.

Where This Leaves Us

Until incentives shift, affordability won’t magically return, and an entire generation will remain shut out of homeownership. The American Dream is no longer about owning a home. It is about owning scarcity. Those who bought before 2020 benefit. Those who didn’t, struggle.

This is one of the most underreported economic stories in America. Housing isn’t a crisis. It’s a wealth transfer machine built by policy and protected by voters.

It’s not broken.

It’s working exactly as designed.